Driven by generative AI (Gen AI) and global digital transformation, surging demand for computing power is comprehensively reshaping how data centers are built and operated. Hyperscale data centers, in particular, have become the main focus of investment and construction.

According to TrendForce, lighting systems, which accounted for less than 2% of total data center construction costs in the past, have now evolved from an overlooked component into an indispensable part of achieving green and low-carbon goals. This shift comes amid strict PUE (Power Usage Effectiveness) regulations and the trend toward zero carbon emissions — for instance, new data centers are required to maintain a PUE below 1.3 or 1.4.

Data Center Lighting

Boosted by the expansion of AI computing power and rising LED penetration, the data center lighting market is enjoying strong growth momentum.

Latest data from TrendForce shows:

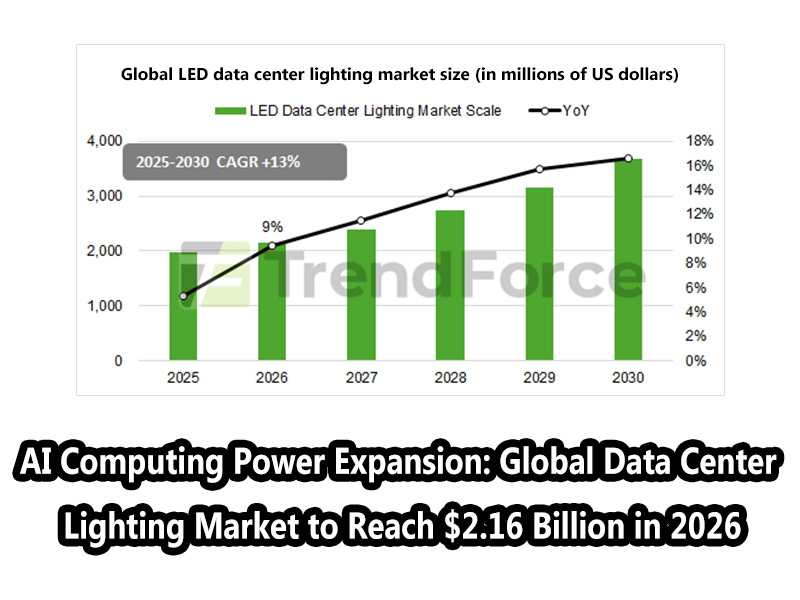

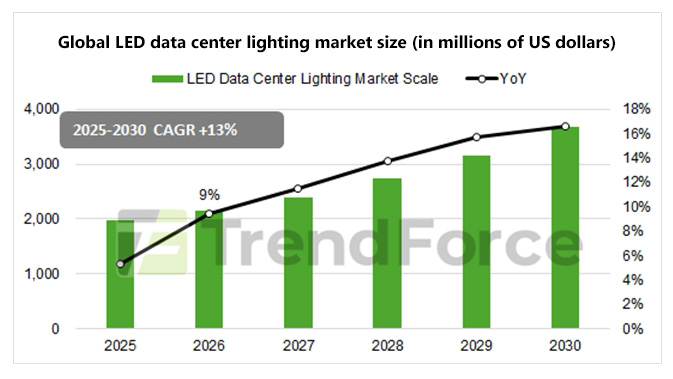

- The global LED data center lighting market reached $1.97 billion in 2025.

- It is projected to expand to $2.16 billion in 2026, representing a year-on-year increase of 9%.

- By 2030, the market size is expected to grow to $3.69 billion, with a compound annual growth rate (CAGR) of 13% from 2025 to 2030.

Regionally, North America remains the world’s largest market, supported by massive replacement and system upgrade demand.

Driven by supportive policies and digital economy investments in China, India, Southeast Asia and other markets, the Asia-Pacific region is entering a new wave of construction and has become the most dynamic growth region.

Critical data center facilities operate 24/7, requiring much higher lighting reliability than general commercial lighting.

To meet extreme energy efficiency requirements, mainstream LED luminaires now typically offer luminous efficacy of over 160 lm/W, effectively reducing the thermal load on cooling systems.

They must also provide a service life of more than 100,000 hours, and use cool white light in the 4000K–5000K range with high color rendering for easy cable identification.

In addition, with the growing popularity of lights-out data centers, smart lighting supporting infrared or microwave sensor dimming has become standard, and demand-based lighting is gaining rapid adoption.

Amid huge market opportunities, the global data center lighting industry has formed a multi-tiered competitive landscape:

- Signify, through Cooper Lighting and its Interact IoT platform, provides full lifecycle solutions including LiFi wireless technology and customized designs, solidifying its position in the high-end ecosystem.

- Acuity Brands has established a strong presence in North America via its intelligent edge strategy, deeply integrating lighting into building management system architectures.

- Zumtobel, with its TECTON continuous trunking system, emphasizes high modularity, tool-free installation and superior light quality, favored by high-end colocation and image-oriented data centers.

- LEDVANCE focuses on general replacement solutions using standardized linear luminaires.

- PacLights specializes in high-ROI retrofits in the existing market, offering magnetic kits and flexible dimming designs for low-cost maintenance.

TrendForce believes data center lighting systems are increasingly integrated into overall infrastructure.

In the future, leading manufacturers with cross-system integration capabilities and EPD (Environmental Product Declaration) certification will continue to expand their influence in the high-end market.

Companies focused on existing facility retrofits and flexible upgrade solutions will also maintain stable positions, as the market becomes increasingly specialized and segmented.

(Source: TrendForce)

This article is reprinted from www.ledinside.cn. If any copyright infringement is involved, please contact us.